The coronavirus relief bill enacted by Congress in March aimed to shield credit scores from the fallout of consumers skipping loan payments due the pandemic. But observers say borrowers benefiting from the provision still face risks.

The legislation aims to treat pandemic-related forbearance plans similar to the relief provided after hurricanes or other natural disasters. Creditors can now attach a "disaster code" to a loan telling the credit bureaus that a consumer was hurt financially by the coronavirus, and their score should be unaffected.

But experts warn that consumers may not realize that their credit reports could still become impaired once a forbearance plan or other type of relief expires.

“As soon as the lender stops reporting with the disaster code, it ostensibly unfreezes the credit report to the consumer and they will be evaluated based on any negative events that happened,” said James Garvey, founder and CEO of Self Financial Inc., a Texas fintech firm that tries to help unbanked consumers build their credit.

Use of such disaster codes has never been so widespread and it is not even clear yet how many borrowers have sought relief. The credit reporting industry plans to release a report in the coming weeks indicating how many of the 220 million consumer credit files have been flagged with a disaster code.

So far, credit reporting advocates say the implementation of the measure in the Coronavirus Aid, Relief, and Economic Security Act is going smoothly.

“We are not seeing a lot of pushback from consumers and it appears that credit reporting under the CARES Act is going well,” said Francis Creighton, president and CEO of the Consumer Data Industry Association, which represents the three major credit bureaus Equifax, Experian and TransUnion.

Yet some borrowers have faced apparent blowback from forbearance plans in their credit files.

The credit score company VantageScore Solutions, a joint venture of the three credit bureaus that offers an alternative to FICO score, notified consumers that their scores may have been impacted from the widespread use of forbearance and deferment codes for consumer loans on which lenders have given payment relief. The Stamford, Conn., company posted a notice on its web site that it made adjustments to its algorithms “to minimize the negative impact associated uniquely with the usage of these codes.”

Even if a borrower’s credit score does not take an immediate hit, many consumers are unaware that having a disaster code on their report will hurt their future ability to access credit.

"Consumers will probably forfeit the ability to refinance their loan or get a new loan for at least three months — and the reason I say ‘probably,’ is because the impact of a forbearance isn’t spelled out anywhere clearly yet,” said Brian S. Levy, of counsel at the Chicago law firm Katten & Temple LLP. “Mortgage lenders will have the unfortunate task of telling many future applicants who used forbearance that they gave up their ability to refinance, cash out, or get new financing for a while.”

Compounding the problem for homeowners is that consumers with loans backed by Fannie Mae and Freddie Mac are eligible to refinance if they are current on their mortgage or in forbearance, and have made three consecutive mortgage payments, the Federal Housing Finance Agency said last month. That policy, however, applies only to loans backed by the government. Investors in private label mortgages do not have to abide by that policy.

Companies have fielded frantic calls from consumers about what happens to credit scores and credit reports when the pandemic is over. The relief bill says that if a creditor makes an accommodation for a consumer, that lender should report the account as current for 120 days.

“I would be worried about what happens after the 120-day period,” said Megan Horner, publisher of banking and credit cards at Finder.com.

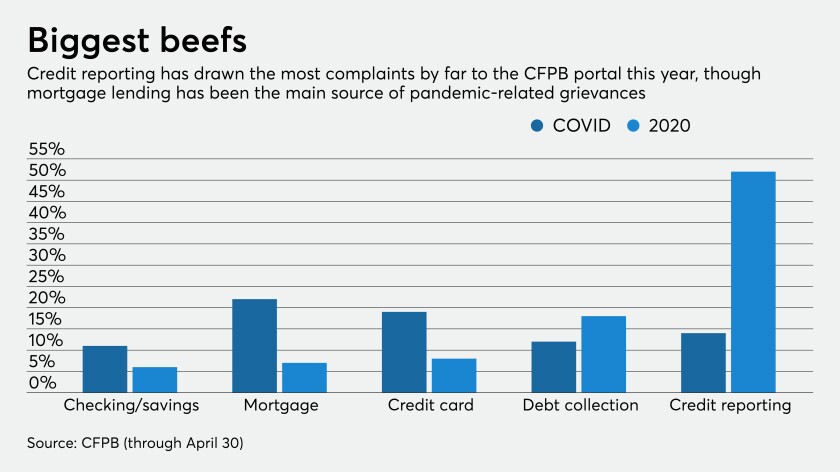

Credit reporting routinely tops the list of complaints to the Consumer Financial Protection Bureau, garnering 52% of all complaints between Jan. 1 and April 30, which far outpaces any other industry. Over half of consumers who complain about the credit bureaus cite having incorrect information listed on their credit report, the CFPB said in a recent report.

Because credit reporting is a lagging indicator, with missed or late payments typically not reported for at least 30 days, the industry is only now starting to get a handle on how many consumers have asked for a forbearance or deferral from a creditor.

A big concern for consumer advocates is that low- and moderate-income consumers may find that they are locked out of credit when the pandemic is over, which is precisely when they need access the most.

“We may see that companies are temporarily not punishing consumers when they are in financial distress and are not actively seeking credit, but when the disaster is over, they might need credit and that’s when they get punished,” said Dan Quan, founder and managing partner of Banks Street Advisory, and a former CFPB senior adviser and head of the bureau’s fintech office.

The CFPB provided guidance in April supporting lenders’ “voluntary efforts” to provide payment relief to consumers. The CFPB also said it will not take enforcement actions against or cite in examinations any company that provides information to credit reporting agencies that accurately reflects payment relief measures.

Some experts think the CFPB should be telling creditors that failing to use the disaster code and abide by the relief bill is a violation of the Fair Credit Reporting Act.

"The need for consumer protections is greater than ever," said former CFPB Director Richard Cordray. "The credit bureaus have said that once we're out of the disaster, people will be held to account retroactively for bills they didn't pay."

Credit reporting is complicated by a range of factors. Algorithms used to compute credit scores are automated and difficult to change. Moreover, a consumer could see his or her credit score drop for reasons that have nothing to do with a forbearance or deferral.

The congressional relief bill mandated that if a consumer has an accommodation from a creditor, such as a forbearance or a deferral, then that trade line is marked as paid and technically listed as current on a credit report. Banks, credit card issuers and auto lenders have largely abided by the congressional intent of the relief bill in using disaster codes and not reporting forbearances as delinquencies.

Creditors do not want to face class-action lawsuits alleging consumers were harmed if they misapply the codes, causing credit scores to nosedive.

So far, only one company has been cited for reporting incorrect information to the credit bureaus that ended up lowering credit scores for millions of borrowers.

The company, Great Lakes Educational Loan Services, released a statement this month saying it was working with the credit bureaus to change how it reports forbearances and to accurately report student loan accounts as current. Great Lakes provided information on nearly 5 million student loan borrowers that in some cases resulted in lower credit scores, the Education Department said this month.

Early on in the crisis, the credit bureaus and other financial firms were successful at stopping legislation that would have put a moratorium on all negative credit reporting during the pandemic. The thinking was that restricting negative credit reporting would result in inaccurate reports, and if lenders cannot rely on the truth of a credit report, they would raise interest rates generally for all consumers.

“One thing to be concerned about is that people might be taking out credit cards or loans right now because they don’t have enough cash, and they may be using those and not able to pay them off after the pandemic is over,” said Horner.

Garvey agreed that "if the credit report is unreliable, it’s no longer valuable for lenders."

"still" - Google News

June 02, 2020 at 08:30AM

https://ift.tt/2ZZYZyr

Coronavirus still a threat to credit scores despite congressional relief - American Banker

"still" - Google News

https://ift.tt/35pEmfO

https://ift.tt/2YsogAP

Bagikan Berita Ini

0 Response to "Coronavirus still a threat to credit scores despite congressional relief - American Banker"

Post a Comment